Each year, the Internal Revenue Service (IRS) updates cost-of-living adjustments, impacting contribution limits for retirement plans as well as various tax deductions, exclusions, exemptions, and thresholds. Here are some of the significant changes for 2025.

Estate, gift, and generation-skipping transfer tax

- The annual gift tax exclusion (and annual generation-skipping transfer tax exclusion) for 2025 is $19,000, up from $18,000 in 2024.

- The gift and estate tax basic exclusion amount (and generation-skipping transfer tax exemption) for 2025 is $13,990,000, up from $13,610,000 in 2024.

Standard deduction

A taxpayer can generally choose to itemize certain deductions or claim a standard deduction on the federal income tax return. In 2025, the standard deduction is:

- $15,000 (up from $14,600 in 2024) for single filers or married individuals filing separate returns

- $30,000 (up from $29,200 in 2024) for married joint filers

- $22,500 (up from $21,900 in 2024) for heads of households

The additional standard deduction amount for the blind and those age 65 or older in 2025 is:

- $2,000 (up from $1,950 in 2024) for single filers and heads of households

- $1,600 (up from $1,550 in 2024) for all other filing statuses

Special rules apply for an individual who can be claimed as a dependent by another taxpayer.

IRAs

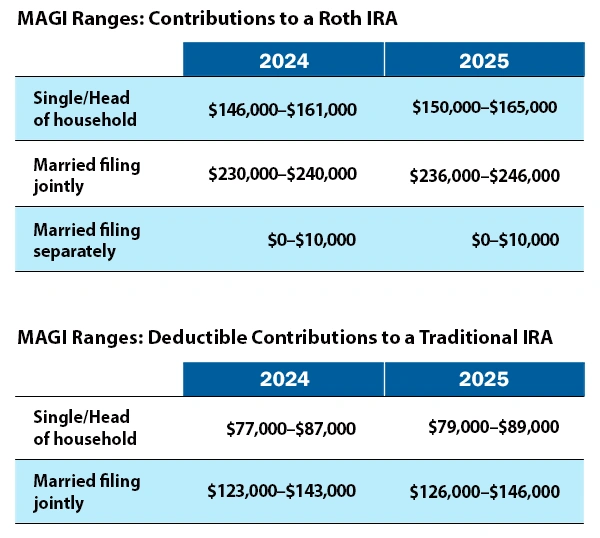

The combined annual limit on contributions to traditional and Roth IRAs remains $7,000 in 2025, with individuals age 50 or older able to contribute an additional $1,000. The limit on contributions to a Roth IRA phases out for certain modified adjusted gross income (MAGI) ranges (see table). For individuals who are active participants in an employer-sponsored retirement plan, the deduction for contributions to a traditional IRA also phases out for certain MAGI ranges (see table). The limit on nondeductible contributions to a traditional IRA is not subject to phaseout based on MAGI.

Note: The 2025 phaseout range is $236,000–$246,000 (up from $230,000–$240,000 in 2024) when the individual making the IRA contribution is not covered by a workplace retirement plan but is filing jointly with a spouse who is covered. The phaseout range is $0–$10,000 when the individual is married filing separately and either spouse is covered by a workplace plan.

Employer-sponsored retirement plans

- Employees who participate in 401(k), 403(b), and most 457 plans can defer up to $23,500 in compensation in 2025 (up from $23,000 in 2024); employees age 50 or older can defer up to an additional $7,500 in 2025 (the same as in 2024), increased to $11,250 in 2025 for ages 60 to 63..

- Employees participating in a SIMPLE retirement plan can defer up to $16,500 in 2025 (up from $16,000 in 2024), and employees age 50 or older can defer up to an additional $3,500 in 2025 (the same as in 2024), increased to $5,250 in 2025 for ages 60 to 63.

Kiddie tax: child’s unearned income

Under the kiddie tax, a child’s unearned income above $2,700 in 2025 (up from $2,600 in 2024) is taxed using the parents’ tax rates.

Source: irs.gov